Key Takeaways:

- The 2026 housing market is stable but slow — prices are holding, not surging, so sellers should expect modest gains rather than a windfall

- Waiting for 2027 is unlikely to pay off significantly; forecasters project gradual improvement, not a dramatic rebound

- Where you live matters more than national headlines — Sun Belt markets face continued softening while Midwest cities show surprising strength

- Lower mortgage rates cut both ways: they bring more buyers and more competing sellers, so timing your listing around rate drops is a risky strategy

- Carrying costs are real — property taxes, insurance, and maintenance accumulate while you wait for a “better” market that may never dramatically arrive

- Federal policy changes around institutional buyers are unlikely to move the needle much on affordability or your sale price

- The biggest driver of when to sell should be your personal circumstances, not market timing — life events, equity position, and home condition matter far more than any forecast

If you’ve been sitting on the fence about selling your home, you’re in good company. Millions of homeowners across the country are asking the same question right now: Is 2026 the window I’ve been waiting for, or should I hold out another year and hope the market looks friendlier in 2027?

Here’s the short answer — and then we’ll break it all down: There is no universally “right” time to sell a home. But the data we have right now tells a pretty clear story about what the market looks like today, what it’s likely to look like next year, and what that means for you specifically.

Spoiler: The era of wild price jumps is behind us. What’s ahead is something more measured — and depending on your situation, that could be either an opportunity or a reason to wait.

The Big Picture: A Market Finding Its Footing

Let’s start with the headline numbers, because they set the stage for everything else.

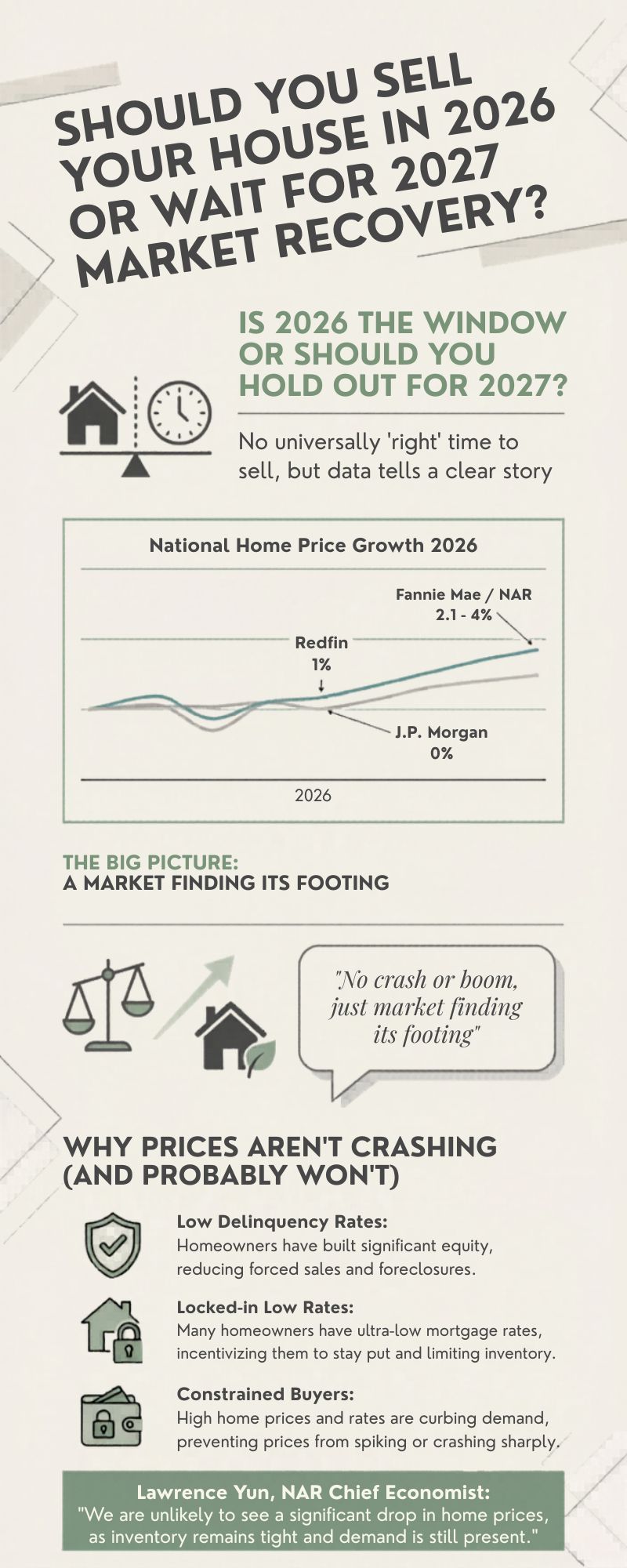

National Prices Are Essentially Flat

National home prices in 2026 are essentially in a holding pattern. J.P. Morgan Global Research projects that U.S. home prices will stall at roughly 0% growth nationally in 2026, with a slight improvement in buyer demand likely offsetting any new supply coming onto the market. In other words, prices aren’t tumbling — but they’re not climbing meaningfully, either.

The More Optimistic Forecasts Still Point to Slow Growth

Redfin’s forecast lands in a similar zone, projecting about 1% year-over-year price growth for the median U.S. home sale in 2026. Their analysts attribute this to still-elevated mortgage rates and a weakening economy that together suppress demand. Meanwhile, Fannie Mae and the National Association of REALTORS® (NAR) are slightly more optimistic, projecting price gains in the range of 2.1% to 4% — which, in dollar terms on a median-priced home around $410,800, translates to somewhere between $9,000 and $16,000 in additional value over the course of the year.

What This Means for Sellers

What does all that mean when you average it out? Most forecasters agree that price growth in 2026 will be slow and modest, nowhere close to the 15–20% annual surges we saw during the pandemic-era boom. As one housing broker put it to CNBC: “There won’t be a crash or a boom, just the market finding its footing after years of extraordinary disruption.”

That’s actually useful information for sellers. A stable, balanced market is far easier to sell into than a chaotic one — you just need to have the right expectations going in.

Why Prices Aren’t Crashing (And Probably Won’t)

Before you decide whether to list or wait, it helps to understand why the market is stabilizing rather than correcting dramatically.

Most Homeowners Simply Aren’t Being Forced to Sell

The biggest reason is simple: most homeowners aren’t being forced to sell. Mortgage delinquency rates are sitting near historic lows, and the majority of existing homeowners locked in ultra-low mortgage rates during 2020–2022. They have significant equity and little financial pressure to offload their properties at a discount. As Redfin’s analysis notes, sellers who might otherwise list their homes are simply choosing to wait, which keeps the supply of existing homes constrained and provides a floor under prices.

The Lock-In Effect Is Keeping Supply Tight

This is a dynamic that plays out as something of a standoff. Buyers are constrained by affordability — high prices combined with mortgage rates that have been stubbornly stuck above 6% for the better part of three years now. Sellers, meanwhile, are constrained by the so-called “lock-in effect,” where trading up or moving means giving up a 2.5% or 3% mortgage for a 6.5% one. Nobody wants to make that trade unless life demands it.

The Experts Agree: There’s a Floor Under This Market

The NAR’s Chief Economist Lawrence Yun has been explicit that nationally, “home prices are in no danger of declining.” His forecast actually calls for a median 4% national price gain in 2026. That may be on the optimistic end of the spectrum, but it underscores a broader consensus: this market has a floor, and sellers aren’t staring down a cliff.

The Regional Story Is Where It Gets Complicated

Here’s where the national averages can be misleading. When you zoom in, the 2026 housing market looks very different depending on where you live.

Sun Belt and West Coast Markets Are Feeling the Pressure

In the Sun Belt — think Florida, Texas, Arizona, and the broader Southwest — there’s a real glut of newly built homes left over from the pandemic construction boom. These markets are among those where prices are actually expected to decline in 2026. According to Realtor.com projections, 22 of the 100 largest U.S. metros are forecast to see year-over-year price drops next year, and the majority of those cities are in the Southeast and West.

J.P. Morgan’s research team specifically called out West Coast and Sun Belt markets as places where “supply is a key factor” in driving price declines. If you own a home in one of these oversupplied areas, 2026 may actually be a year where waiting gets you a lower price, not a higher one.

The Midwest Is a Different Story Entirely

On the flip side, markets in the Midwest — places like Columbus, Ohio, Indianapolis, and Kansas City — are showing real resilience and even strength. These areas have long been more affordable, which insulates them from the affordability squeeze hammering coastal markets. If you’re selling in one of these cities, the calculus is different.

The bottom line: national data is a starting point, not a verdict. Your local market dynamics will matter far more than the national trend line.

What Mortgage Rates Are Doing (And Why It Matters for Sellers)

You might be thinking: “If rates drop, more buyers will show up. Shouldn’t I wait for that to happen?”

It’s a reasonable instinct, but there’s a catch — and it’s one that most sellers overlook.

Rates Are Down from Their Peak — But Still Elevated

Current 30-year fixed mortgage rates are hovering around 6.2–6.3%, down from the 7%+ highs of 2023 but still historically elevated. Realtor.com projects rates averaging around 6.3% through 2026, while Zillow expects them to hover just above 6%. The general consensus is that rates won’t drop dramatically — the Federal Reserve isn’t expected to cut aggressively, especially given lingering inflation concerns.

Builder Incentives Are Already Picking Up the Slack

J.P. Morgan and other analysts note that adjustable-rate mortgages (ARMs) could tick lower if the Fed eases, and homebuilders are increasingly offering rate buydowns — essentially paying upfront to lower a buyer’s mortgage rate — to move inventory. These buyer incentives are already nudging demand higher.

Lower Rates Bring More Sellers Too — Not Just More Buyers

Here’s the catch when it comes to waiting for rates to fall: lower rates bring more buyers back into the market, yes. But they also bring more sellers. If you’re banking on a big rate drop in 2027 to supercharge your sale price, you may find yourself competing against a wave of other sellers who had the same idea. The increased supply that accompanies improved buyer demand can neutralize the pricing benefit you were hoping to capture.

The advice that keeps showing up from real estate professionals: don’t try to time the market based on rate movements alone. It’s an unpredictable variable, and chasing it can cost you more than it saves.

Federal Policy: Big Headlines, Limited Impact

If you’ve been following housing news in early 2026, you’ve probably seen the headlines about the Trump administration’s proposed ban on large institutional investors buying single-family homes. It’s a significant policy announcement, and it’s understandably generating buzz.

But here’s some context that’s worth keeping in mind: while institutional buyers — large corporations and investment funds that purchase homes to rent them out — have played a meaningful role in tightening inventory in some markets, they represent a relatively small share of total home purchases nationally. Policy experts have broadly noted that restrictions on institutional buyers are unlikely to dramatically shift overall home prices or affordability in the short term.

The Real Affordability Problem Runs Deeper

The research backing this is consistent with broader housing policy analysis suggesting that restrictions on institutional buyers or mortgage-backed security purchases tend to have a “minimal impact on lowering overall costs.” The core affordability problem isn’t institutional buyers hoarding inventory — it’s the fundamental mismatch between the number of homes available and the number of households that want to own one. The only real solution to that is building more homes, and that’s a multiyear process.

Don’t Let Policy Headlines Drive Your Selling Timeline

For sellers, this means you shouldn’t be making your timing decision based primarily on policy interventions. They may reshape the market at the margins, but they won’t be the thing that makes 2027 dramatically better or worse than 2026.

The Case for Selling in 2026

Alright, so given everything above — what’s the actual argument for listing your home this year rather than waiting?

There are several compelling ones.

You’re selling near the top of the cycle.

Home prices have nearly doubled over the past decade, and they’ve largely held their ground even as the market cooled. The rapid appreciation phase is over, and NAR economists confirm that the era of outsized price gains is transitioning into something more like equilibrium. If you’ve owned your home for five or more years, you’ve almost certainly built substantial equity. Selling now locks that in.

Competition from other sellers is still manageable.

Inventory is rising but remains well below pre-pandemic norms. As of late 2025, inventory was about 15% higher than a year earlier — which sounds like a lot, but housing supply is still nowhere near the levels that would give buyers significant leverage in most markets. You’re not selling into a flooded market, at least not yet.

Buyer demand is showing signs of life.

Mortgage applications have been trending meaningfully above last year’s levels. NAR’s Yun noted that in one recent week, purchase mortgage applications were up 31% compared to the same period a year prior. That’s not a sign of a dead market — that’s genuine buyer interest starting to reassemble.

Sales activity is projected to increase.

Existing-home sales are forecast to rise modestly to around 4.13 million units in 2026, up from roughly 4.07 million in 2025. NAR’s chief economist is even projecting a 14% nationwide increase in home sales. More transactions in the market means more buyers circulating, which is good news for sellers.

The longer you wait, the more carrying costs add up.

While you’re waiting for 2027 to materialize, you’re still paying property taxes, insurance, maintenance, and potentially a mortgage. Those costs don’t pause. A gain “probability” in 2027 competes against real, concrete costs you’re paying right now.

Spring 2026 is a real opportunity.

Historically, spring is the best time of year to sell a home. Buyer activity peaks, homes photograph better with natural light and blooming yards, and families are motivated to close before the school year starts. The spring 2025 season was hobbled by mortgage rates sitting around 6.8%. This spring, with rates closer to 6.3%, the conditions are meaningfully better.

The Case for Waiting Until 2027

Okay, to be fair — there are also legitimate reasons to wait, and we’d be doing you a disservice if we didn’t lay them out.

If you’re in an oversupplied market, prices may recover later.

In Sun Belt cities where new construction has outpaced demand, 2026 may actually be the low point. If you can afford to ride it out, there’s a reasonable argument that conditions in 2027 could be somewhat more favorable as that excess inventory gets absorbed.

Affordability is slowly improving.

Redfin’s forecast notes that 2026 will mark the beginning of a period where income growth outpaces home-price growth — which should gradually bring more buyers off the sidelines. The pool of qualified buyers is expected to expand over time. If you wait another year, you may be selling into a broader pool of buyers.

If your home needs significant work, waiting to prepare it properly is smart.

A well-prepared home outperforms a rushed listing. If you’re planning major repairs or updates, taking the time to do them properly — and listing when the home is in its best condition — can offset the cost of waiting.

Life circumstances should drive the decision more than markets.

Zillow’s research found that 78% of sellers say a major life event — a new job, a change in family size, a divorce, retirement — was the primary driver of their decision to move. If you’re not in a situation that necessitates selling, there’s no law requiring you to act in any particular year.

The 2027 Question: What Are We Actually Waiting For?

Here’s the thing about the “2027 market recovery” narrative: most forecasters expect a gradual improvement in housing conditions over the next several years, not a dramatic rebound in any single year.

U.S. News and World Report’s five-year housing forecast projects GDP growth remaining muted at 1.6% to 1.8% through 2026–2027, with home prices rising slowly and mortgage rates staying elevated unless there’s a significant economic shock. Fannie Mae expects moderate price growth in 2027 similar to 2026 levels. This isn’t a recovery that arrives in a wave — it’s more of a slow tide coming in.

The phrase “market recovery” can be misleading because it implies that the current market is broken and something dramatically better is around the corner. It isn’t. What analysts actually project for 2027 is a continuation of the gradual normalization already underway — incrementally more sales, incrementally better affordability, incrementally lower rates. It’s a market getting better, not a market getting hot.

If you’re waiting for 2027 expecting to sell in conditions significantly more favorable than today’s, the data doesn’t strongly support that expectation. The improvement is likely to be marginal, and it comes with the added risk that your local market could move in an unexpected direction.

What Should Actually Drive Your Decision

Strip away all the data and forecasts, and the honest truth is that the best time to sell a house is when it makes sense for your specific situation. Here’s a practical framework for thinking it through:

Sell in 2026 if:

- You’ve built significant equity and want to capture it while prices are stable

- You’re in a local market with strong demand and limited inventory

- Life circumstances are pushing you toward a change (job relocation, family size, downsizing, retirement)

- Your home is move-in ready or close to it

- You’re in a Sun Belt market where further price softening is possible

Consider waiting if:

- Your home needs substantial preparation before it can command top dollar

- You’re in a market where inventory is rising sharply and buyers have leverage

- You have no particular need to move and are financially comfortable holding

- You’re watching for a specific local development (infrastructure, employer arrival) that could boost your neighborhood’s value

Either way, the most important step is getting a clear picture of what your home is actually worth right now in your specific market — not what national headlines say, but what comparable homes in your zip code are actually selling for. From there, you can make a decision based on facts, not fear or speculation.

The Bottom Line

The 2026 housing market isn’t the seller’s paradise of 2021, and it’s not a buyer’s market either. It’s a balanced, transitional market — more competitive than sellers would like, more expensive than buyers can easily handle, but fundamentally stable.

Prices are holding. Buyer demand is cautiously returning. Inventory is rising, but not flooding. And the fever dream of 20% annual appreciation is clearly over.

For most sellers, 2026 offers a reasonable window — particularly in the spring and early summer months when buyer activity historically peaks. The case for waiting until 2027 exists, but the data doesn’t support the idea that next year will be dramatically more favorable. Gradual improvement, yes. A transformed market, no.

The best move? Talk to a local real estate professional who knows your specific market. Get a comparative market analysis done on your home. Understand what it would actually sell for today. Then make your decision based on your real financial picture and your real life circumstances — not on the hope that the market will do something dramatic in twelve months that the experts aren’t currently projecting.

Because here’s the thing about trying to perfectly time the housing market: it almost never works. What does work is being ready, being informed, and moving when the time is right for you.